3D Printing and Printed Materials in 2020: A Challenging Year But Fascinating Times Ahead, Reports IDTechEx

Although 3D printing as a technology has been around for several decades, it has made serious headway into factories, homes, and offices since the patents for the fused deposition modeling (FDM) printing process expired in 2009. In the years have that followed, 3D modeling has become increasingly popular – in homes for hobbyists and in industry, particularly for prototyping and the early phases of product development. But in 2020, the landscape began to change once more.

Although the COVID-19 pandemic has interrupted the 3D printing sector and its end users (such as printing bureaus), new directions of travel have nonetheless emerged. Some opportunities have even been directly prompted by the pandemic.

3D printing and the fight against COVID-19

In late 2019/early 2020, health systems in much of the world went onto a war footing as the COVID-19 pandemic took hold. Demand for PPE and medical peripherals like filters and swabs went through the roof, but 3D printing was well placed to respond – and it did. Italian company Isinnova developed a 3D-printed connector, the Charlotte valve, which could be used to fit a commercial snorkeling mask to CPAP machine; this was swiftly followed by 3D-printed swabs and personalized 3D-printed face masks. Even emergency dwellings to isolate quarantined patients were printed. All of these were gratefully received but highlighted an issue that continues to plague the sector: a lack of regulatory control and standardization within 3D printing as a whole made it difficult for printed medical devices to gain the approvals required for use as medical devices. This, in turn, limited the extent to which they could be used.

However, the expanding range of materials used in printing, along with the experience granted by COVID-19, has alerted many people to the potential of 3D printing in healthcare. In particular, the ability to produce specialist, customized items on demand is attractive because it reduces waste and inventory throughout the supply chain. While traditional plastic filaments may be of limited use, given their fragility and issues around infection control, the increasing use of metal and bio-printing is opening up a world of possibilities.

COVID-19 has also shown the advantages of 3D printing in terms of speed, customization, and increasing versatility, along with reliable production (if one printer in a bureau breaks, there will be several others than can quickly take on its work – this is generally not the case in traditional manufacturing). Sales of industrial-scale printers plummeted as the world went into lockdown, but printer manufacturers may be comforted by a growing number of applications in the longer term. Meanwhile, sales of home printers soared as people stuck at home sought hobbies to pass the time.

Plastics – down, but not out

Printing with plastics has been less dominant in 2020, but this is not the end for traditional filaments (powders have been less affected), and IDTechEx foresees a rebound in due course. Meanwhile, the 3D sector as a whole is shifting, and in particular, more companies are integrating 3D printing into general manufacturing processes as well as prototyping. This calls for a wider range of printing materials and printers, depending on the components or processes involved.

A key market driver is sustainability, with several consumable firms investigating bio-sourced materials – not merely to enhance biocompatibility in medical or research settings but also to produce 'greener' biodegradable end products, including packaging.

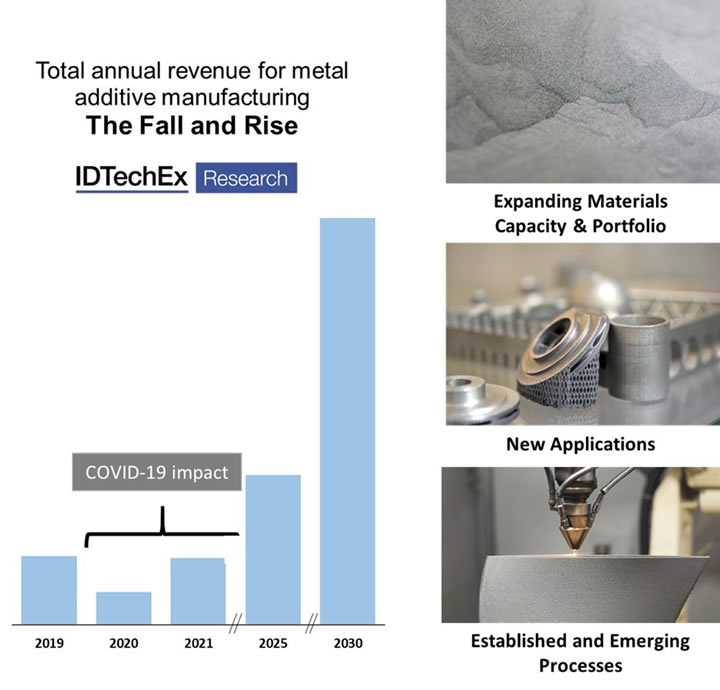

While plastics are widely acceptable for prototyping, the same is not true for all components or end products, so newer materials are of interest to all concerned. The world market for metal components, for example, is worth trillions of dollars each year, and 3D printing meets many end-users' requirements for customizable, decentralized production.

Thus, 2020 has seen interest in metal additive manufacturing, in particular with aluminum alloys and steel. Titanium, Cobalt-chrome, and other emerging variants are particularly used for medical printing due to longevity and biocompatibility requirements. Some companies have now produced and protected proprietary consumables, such as liquid metal, as production scales up. The increasing appetite for new printing materials coincides with the development of printers that can create larger items, and together these are meeting the diverse and growing demands of multiple sectors for 3D printed products.

Then there is the exciting field of composites that are gaining notable traction. IDTechEx has seen an increasing number of players, demonstrations, and partnerships expanding from the 2019 news surrounding Markforged and Desktop Metal. The most notable announcement being the $48.5m Series B funding raised by Arris Composites. However, any growth may not be immediate, thanks to the influence of COVID-19.

Aerospace and automotive – key markets disrupted by COVID-19

Aerospace is an important market for 3D printing, especially with metal, and many commercial airliners now have printed components and have been looking for more. An increasing number of appropriate printing materials (primarily alloys) have come to market, and both 3D printing technologies and materials have now evolved to the point that alloy proportion and composition can be varied across the component, and larger components can be printed.

The advantages of 3D printing for aerospace lie in saving weight (which in turn saves huge amounts in fuel costs), reducing the buy-to-fly ratio, or in customizable, on-demand, and decentralized manufacture. For similar reasons, automotive is another key market for 3D printing.

Binder jetting has continued to gather attention across 2020, Desktop Metal has undergone a merger and is live on the New York Stock Exchange, raising even more funding, GE Additive announced more partnerships, including Sandvik, and HP announced more users. However, aerospace has been devastated by the COVID-19 pandemic, and automotive has also suffered. With vaccination programs now being rolled out, the speed at which both sectors recover will have knock-on effects for makers of 3D printing materials and for printing bureaus. Clearly, both of these will affect the consumables market.

Without a doubt, 2020 has been challenging for 3D printing and consumables as it has been for many sectors, but there is plenty left to play for. More and more companies are finding uses for additive manufacturing, and the technology is maturing beyond product development and into mainstream manufacturing. The demand for metal prints is such that metal printing materials look set to equal or overtake plastics and resin, and new players are entering the field, while bio-inks are at a much earlier stage of development but show great potential. However, despite the influx of new products, plastics have a long-term future and are likely to bounce back from 2020 levels as the market and technologies mature.

For the full portfolio of 3D research available from IDTechEx please visit www.IDTechEx.com/Research/3D.

IDTechEx guides your strategic business decisions through its Research, Subscription and Consultancy products, helping you profit from emerging technologies. For more information, contact research@IDTechEx.com or visit www.IDTechEx.com.

Comments (0)

This post does not have any comments. Be the first to leave a comment below.

Featured Product